Endoscopy devices industry data book covers endoscopes, endoscopy visualization system, endoscopy visualization component and endoscopy operative devices market.

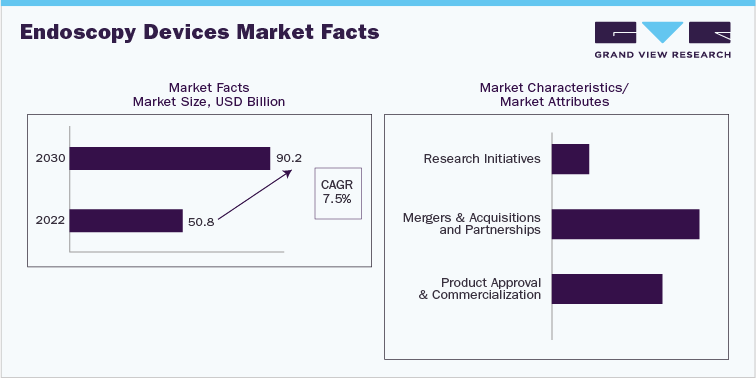

The global endoscopy devices market was valued at USD 50.8 Billion in 2022 and is anticipated to grow at a CAGR of 7.5% over the forecast period.

Grand View Research’s endoscopy devices industry data book is a collection of market sizing information & forecasts, trade data, pricing intelligence, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports and summary presentations on individual areas of research along with an endoscopy devices statistics e-book.

Endoscopes Market Insights

The global endoscopes market was valued at USD 18.8 Billion in 2022 and is anticipated to grow at a CAGR of 9.0% over the forecast period. The rise in prevalence of chronic disorders and the growing awareness of early detection of diseases through minimally invasive surgical procedures are some of the major factors anticipated to drive the market growth over the forecast years. In addition, favorable reimbursement policies, and increasing FDA approvals for endoscopic devices are also expected to boost the growth of the market over the years. For instance, in 2021, the United States Food and Drug Administration granted 510(k) clearance to EndoFresh’s disposable digestive endoscopy system, a device developed to reduce the chance of contamination in gastrointestinal procedures.

North America led the market in 2022 and accounted for the highest share of more than 41.4% of the global revenue. The regional market is estimated to retain the dominant position throughout the forecast period owing to the increasing adoption of elective endoscopic procedures, improved healthcare expenditure, and the high geriatric population. In addition, the high burden of cancer and functional gastrointestinal disorders in the U.S. is anticipated to further drive the market over the forecast period. Asia Pacific is projected to be the fastest-growing regional market over the forecast period. This growth is owing to the presence of a large patient population pool suffering from functional gastrointestinal disorders.

Endoscopy Visualization Component Market insights

The global endoscopy visualization component market was valued at USD 6.7 Billion in 2022 and is anticipated to grow at a CAGR of 7.0% over the forecast period. A significant increase in the number of endoscopic operations, as well as an increasing demand for minimally invasive treatments, are primary factors driving market growth. Endoscopy is becoming more popular due to its advantages over invasive procedures, significant cost savings, and favorable government reimbursement schemes. Furthermore, the increasing adoption of new diagnostic instruments has resulted in an increased demand for advanced visualization approaches. As a result, several manufacturers are emphasizing the introduction of components with enhanced visualization capabilities.

Order Free Sample Copy of Endoscopy Devices Industry Data Book, published by Grand View Research

Endoscopy Visualization System Market Insights

The global endoscopy visualization system market was valued at USD 16.7 Billion in 2022 and is anticipated to grow at a CAGR of 6.8% over the forecast period. Endoscopy is a minimally invasive procedure used for the examination of the internal organs in the body. Visualization systems with advanced technologies can provide superior image quality, which makes them very important in the medical field. In recent years, endoscopic procedures have emerged as a potential adjunctive tool in various medical specialties such as general surgery, gastrointestinal, urology, and others. According to the Centers for Disease Control and Prevention, around 494,000 hysterectomies are performed in the U.S. annually. Approximately 80.0% of the surgeries are done laparoscopically or robotically. Thus, shift towards minimally invasive surgeries and increasing prevalence of cancer, thereby fueling the market growth.

North America dominated the endoscopy visualization systems market and accounted for the largest revenue share of 43.3% in 2020. The rapid adoption of minimally invasive procedures, high prevalence of gastric and colorectal cancer, and growing demand for advanced diagnostic tools are factors attributable to the dominant share of the region in the market. Asia Pacific is projected to witness remarkable growth over the forecast period owing to the high presence of age population in Asian countries such as China, India, and others. In Europe, the market is poised to surge owing to the rising cost burden of cancer and the growing number of endoscopic procedures.

Endoscopy Operative Devices Market Insights

The global endoscopy operative devices market was valued at USD 8.6 Billion in 2022 and is anticipated to grow at a CAGR of 5.7% over the forecast period. The increasing prevalence of chronic disorders, such as obesity, diabetes, and cancer, coupled with the growing geriatric population, is expected to boost the demand for endoscopies. The rising awareness regarding the benefits associated with minimally invasive procedures, such as lesser post-operative complications and shortened hospitalization and recovery time, is further surging the demand for these procedures. The rising incidence of urological, respiratory, gastrointestinal, and gynecological disorders requiring endoscopy for diagnosing and treating the disorders is expected to propel the market growth.

North America accounted for the largest revenue share of over 40.0% in 2020 due to the growing prevalence of cancer and other chronic disorders. The growing preference for minimally invasive procedures using advanced endoscopy operative devices is contributing to the market growth. In addition, the growing demand for endoscopies for diagnostic and therapeutic purposes is propelling the market growth. Asia Pacific is anticipated to register the fastest growth rate during the forecast period due to the growing economies of India and China and rising disposable income in these countries. The increasing prevalence of chronic disorders, growing geriatric population, developing healthcare infrastructure, and the introduction of advanced endoscopic procedures are expected to drive the Asia Pacific market over the forecast period.

Go through the table of content of Endoscopy Devices Industry Data Book to get a better understanding of the Coverage & Scope of the study.

Endoscopy Devices Industry Data Book Competitive Landscape

Increasing demand for endoscopy devices is increasing competition in the market and, thus, forcing key players to introduce new products in the market. Additionally, it is projected that rising industry consolidation activities, such as acquisitions and mergers by the leading market participants, as well as expanding efforts in R&D of endoscopy device applications by key players, are also expected to boost the market share.

Key players operating in the endoscopy devices industry are –

• Olympus Corporation

• Ethicon Endo-surgery, LLC.

• FUJIFILM Holdings Corporation

• Stryker Corporation

• Boston Scientific Corporation

• Karl Storz GmbH & Co. KG

• Smith & Nephew Inc.

• Richard Wolf GmbH

• Medtronic Plc (Covidien)

• PENTAX Medical

• Machida Endoscope Co., Ltd