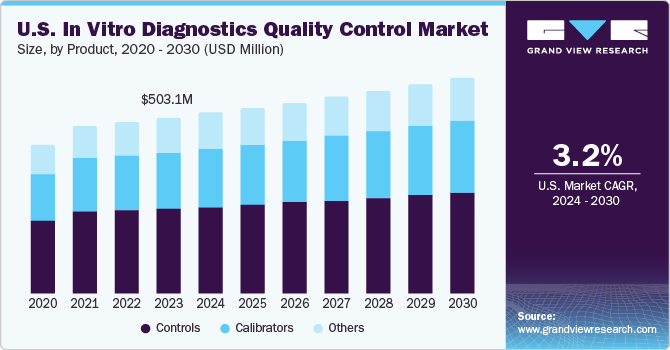

The global IVD quality control market size is expected to reach USD 1.24 billion by 2026, according to a new report by Grand View Research, Inc. The market is projected to witness a CAGR of 4.1% over the forecast period. Continually evolving technology-oriented changes in the diagnostics field and growing need to ensure patient safety necessitate the implementation of quality assurance programs in various medical disciplines including radiology and Point-of-Care (PoC) devices. Patients rely on self-testing IVD devices for long-term disease management and hence it is important for such devices to be checked, in terms of result reproducibility and validity, to guarantee patient safety.

Rising number of certified clinical laboratories offering dependable IVD-based diagnostic services directly correlates with increased patient confidence, thus driving the market. In addition to quality assessments, amendments to the regulatory framework are made intermittently to enhance the existing standards with the main objective of safeguarding qualitative superiority of the diagnostic services. In May 2016, the European Union passed an agreement to update the pre-existing regulations pertaining to IVD devices, wherein the updates were in concern with raising the patient safety levels, particularly for disabled persons. The presence of third-party agencies for independent assessment of the IVD devices is expected to elevate the current safety standards, which will drive the In Vitro Diagnostics (IVD) Quality Control market further.

Further key findings from the study suggest:

- In 2018, the clinical chemistry was the second-largest application segment of the global IVD market, in terms of market share

- Demand for preventive medicine and rapid transformation of clinical laboratories into highly automated and efficient businesses are some of the factors for the segment’s growth

- Molecular diagnostics is projected to be the fastest-growing segment due to increasing technical complexity of molecular diagnostic testing and need for quality evaluation to ensure standards

- These tests are of prime importance as the outcomes enable healthcare practitioners make critical treatment decisions

- Hospitals was the largest segment in 2018 due to the presence of advanced technology-based devices like Next Generation Sequencing (NGS) and microarrays, and rising applications of the optimized quality-control procedures

- North America was the dominant regional market in 2018 due to the presence of over 150,000 registered diagnostics labs and is likely to maintain the dominance throughout the forecast years

- Siemens Healthcare GmbH; Roche Diagnostics; Alere, Inc.; Abbott Laboratories, Inc.; Qiagen N.V.; Bio-Rad Laboratories, Inc.; Quidel Corp.; Becton, Dickinson and Company; bioMerieux, Inc.; Sysmex Corp.; Sero AS; and Thermo Fisher Scientific, Inc. are some of the key companies in the global market

The global In Vitro Diagnostics (IVD) and IVD quality control market combines to account for USD 112.79 billion in revenue in 2021, which is expected to reach USD 114.73 billion by 2030, growing at a cumulative rate of 0.2% over the forecast period. The combination bundle is designed to provide a holistic view of these highly dynamic market spaces.

In Vitro Diagnostics Quality Control Market Segmentation:

Grand View Research has segmented the global IVD quality control market on the basis of application, type, end use, and region:

IVD Quality Control Application Outlook (Revenue, USD Million, 2014 - 2026)

- Immunochemistry

- Hematology

- Clinical Chemistry

- Molecular Diagnostics

- Coagulation

- Microbiology

- Others

IVD Quality Control Type Outlook (Revenue, USD Million, 2014 - 2026)

- Quality Control

- Quality Controls, by Type

- Plasma-based Control

- Serum-based Control

- Whole Blood-based Control

- Others

- Quality Controls, by Application

- Immunochemistry

- Hematology

- Clinical Chemistry

- Molecular Diagnostics

- Coagulation

- Microbiology

- Others

- Quality Assurance Services

- Immunochemistry

- Hematology

- Clinical Chemistry

- Molecular Diagnostics

- Coagulation

- Microbiology

- Others

- Data Management

- Clinical Chemistry

- Immunochemistry

- Hematology

- Molecular Diagnostics

- Coagulation

- Microbiology

- Others

- Quality Controls, by Type

IVD Quality Control End Use Outlook (Revenue, USD Million, 2014 - 2026)

- Hospitals

- Laboratories

- Home-care

- Others

IVD Quality Control Regional Outlook (Revenue, USD Million, 2014 - 2026)

- North America

- S.

- Canada

- Europe

- K.

- Germany

- France

- Spain

- Italy

- Russia

- Asia Pacific

- Japan

- China

- India

- South Korea

- Singapore

- Australia

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

Order a free sample of this Intelligence study @ https://www.grandviewresearch.com/sector-report/in-vitro-diagnostics-ivd-quality-control-industry-data-book/request/rs1