Hemoglobinopathies Industry Overview

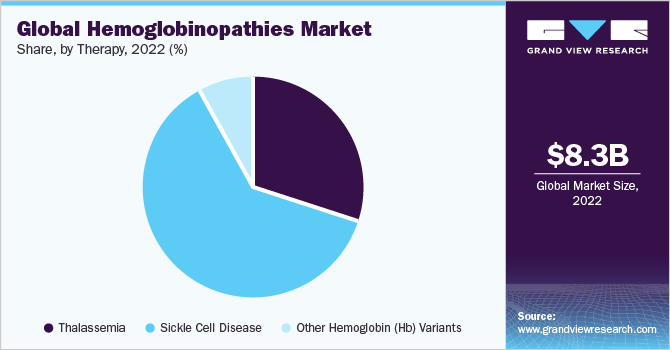

The global hemoglobinopathies market size is expected to reach USD 15.7 billion by 2028, according to a new report by Grand View Research, Inc. It is expected to expand at a CAGR of 10.8% from 2021 to 2028. Increasing awareness regarding hemoglobinopathies and government initiatives to diagnose the diseases at an early stage are expected to propel the market growth over the forecast period. Moreover, increasing R&D investment, the presence of a promising drug pipeline, and technologically advanced diagnostics platforms are expected to boost the growth of the market.

Hemoglobinopathies Market Segmentation

Grand View Research has segmented the global hemoglobinopathies market on the basis of type, diagnosis, therapy, and region:

Based on the Type Insights, the market is segmented into Thalassemia, Sickle Cell Disease, Other Hemoglobin (Hb) Variants.

- The sickle cell disease segment held the largest share of 56.6% in 2020 and is expected to grow at the fastest rate during the forecast period.

- This is attributed to growing initiatives by biopharmaceutical companies and nonprofit organizations focused on improving access to SCD treatment. Furthermore, sickle cell disease affects around 300,000 newborns annually. An estimated 10% to 40% of the individuals in many African countries are carriers of sickle cell gene, which has resulted in a prevalence of around 2% in these countries.

- The thalassemia segment is further sub-segmented into alpha-thalassemia and beta-thalassemia. Globally, 5% of the total population are carriers of alpha-thalassemia and around 1.5% of the population have beta-thalassemia traits. India has the maximum number of thalassemia carriers in the world.

Based on the Diagnosis Insights, the market is segmented into Thalassemia, Sickle Cell Disease, Other Hemoglobin (Hb) Variants.

- The sickle cell disease diagnosis segment dominated the market and accounted for more than 50.0% share in 2020 owing to high diagnostic rates in North America and Europe.

- Blood tests are most widely used for the diagnosis of SCD in patients. Moreover, the introduction of newborn baby screening programs for sickle cell disease in countries, such as the U.S., France, and Italy, will drive the segment at the fastest rate.

- The thalassemia diagnosis segment is estimated to grow at a significant rate over the forecast period. The introduction of technologically advanced, rapid, and user-friendly diagnostic tests is driving the segment.

Based on the Therapy Insights, the market is segmented into Thalassemia, Sickle Cell Disease, Other Hemoglobin (Hb) Variants.

- The sickle cell disease segment held the largest revenue share of 59.4% in 2020. Extensive research has been carried out to develop novel therapies for treating the disorder, which is contributing to the segment growth.

- Gene therapy has emerged as a promising treatment option for managing the disorder as it targets the underlying genetic cause of the condition through one-time administration and reduces the need for patients to undertake blood transfusions.

- Blood transfusion is considered to be the first line of treatment for hemoglobin disorders. The frequency of blood transfusion is higher in thalassemia cases as compared to other hemoglobinopathies. The transfusion is done every 3 to 4 weeks to help maintain the normal level of blood components.

- Bone marrow transplant (BMT) therapy is expected to expand at a significant growth rate over the forecast period. BMT is often used when blood transfusion and other therapies fail. BMT is reported to be effective when performed in the early stages of disease progression.

Hemoglobinopathies Regional Outlook

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa (MEA)

Key Companies Profile & Market Share Insights

Market players are taking up various initiatives, such as mergers & acquisitions, partnerships, collaborations, and extensive R&D, in order to gain a greater share in the market.

Some prominent players in the global hemoglobinopathies market include

- Sangamo Therapeutics, Inc.

- Global Blood Therapeutics, Inc.

- bluebird bio, Inc.

- Emmaus Life Sciences Inc.

- Pfizer, Inc.

- Novartis AG

- Prolong Pharmaceuticals, LLC

- Bioverativ Inc.

- Gamida Cell

Order a free sample PDF of the Hemoglobinopathies Market Intelligence Study, published by Grand View Research.